Innovex International (INVX)·Q4 2025 Earnings Summary

Innovex International Surges 7% to 52-Week High on Strong Q4 Revenue Beat

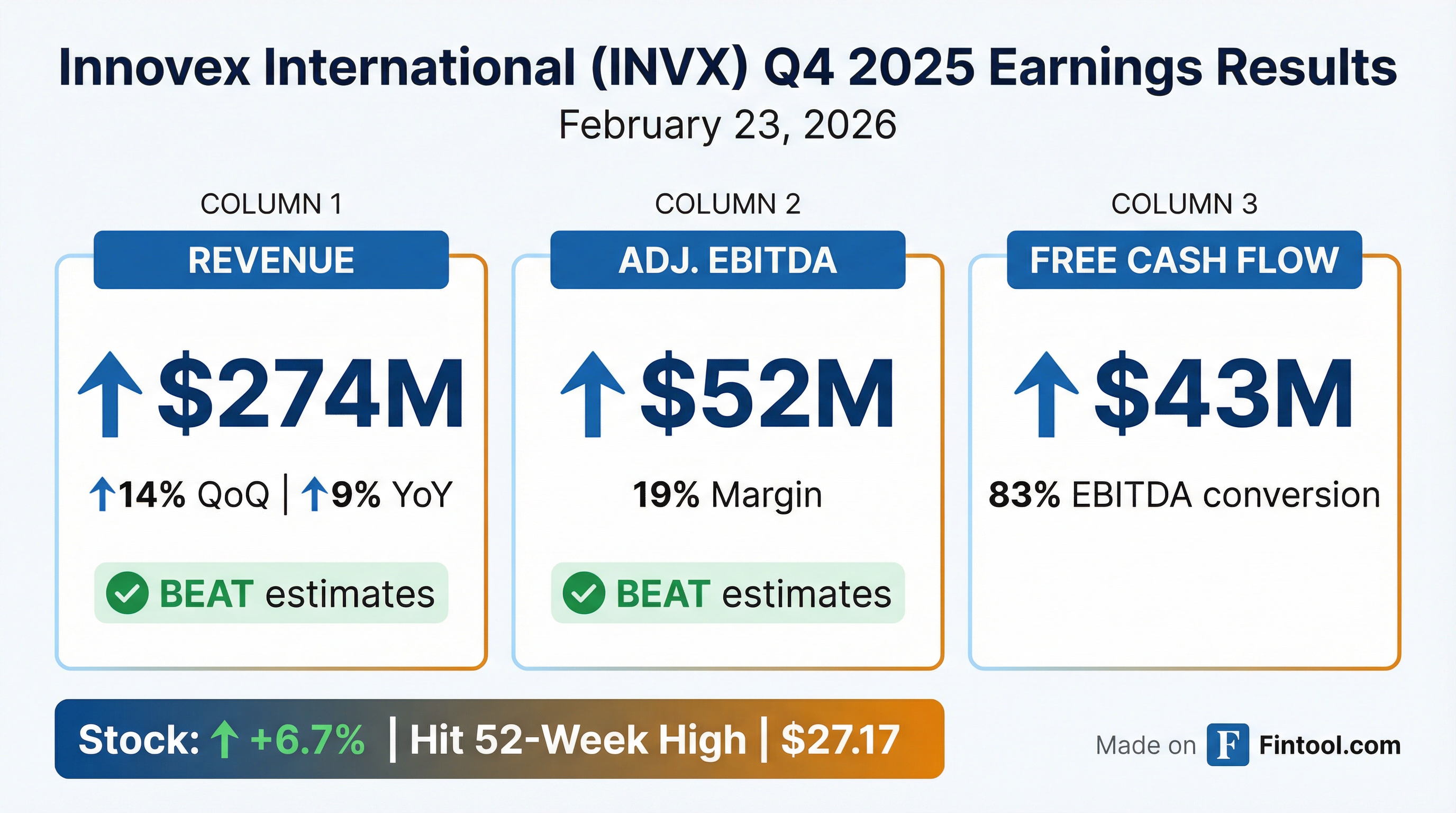

February 23, 2026 · by Fintool AI Agent

Innovex International (INVX) delivered a strong Q4 2025, posting revenue of $274M (up 14% sequentially and 9% year-over-year) with Adjusted EBITDA of $52M at a 19% margin . The oilfield services company generated $43M in free cash flow, converting 83% of Adjusted EBITDA to cash, and ended the year with $203M in cash and no bank debt . The stock surged 6.7% to hit a new 52-week high of $27.28. However, Q1 2026 guidance came in below consensus at $225-235M revenue (vs. $240M expected) and $38-42M EBITDA (vs. $45M expected), reflecting lower subsea deliveries and normal seasonality .

Did Innovex Beat Earnings in Q4 2025?

Yes — Innovex beat on revenue and EBITDA.

*Consensus estimates from S&P Global

The revenue beat was driven by continued strength in International & Offshore markets (49% of Q4 revenue), higher-than-expected subsea deliveries, and revenue synergies from the DWS and Citadel acquisitions .

What Did Management Guide?

Q1 2026 guidance came in below consensus, driven by lower subsea deliveries and normal seasonality.

*Consensus estimates from S&P Global

CFO Kendal Reed explained: "The sequential revenue decrease is primarily due to lower subsea deliveries, reflecting normal seasonality as well as the earlier-than-anticipated execution of certain deliveries originally planned for the first quarter."

Management expects low-margin subsea projects to continue weighing on margins in H1 2026, with improvement expected by year-end following the Eldridge facility exit .

How Did the Stock React?

INVX shares surged +6.7% to $27.17 following the earnings release, hitting a new 52-week high (prior high was $25.55 intraday). Volume was 1.5M shares, approximately 4x the average daily volume.

Key price levels:

- 52-week high: $27.28 (hit today)

- 52-week low: $11.93

- 50-day moving average: $23.87

- 200-day moving average: $19.09

The strong stock reaction reflects investor enthusiasm for the operational transformation and continued revenue momentum heading into 2026.

What Changed From Last Quarter?

Revenue acceleration — Q4's $274M was a 14% sequential jump from Q3's $240M, reversing the softness seen in Q2 ($224M). This marks the highest quarterly revenue in 2025 .

EBITDA margin stability — Maintained 19% Adjusted EBITDA margin despite higher integration costs from recent acquisitions .

Free cash flow strength — $43M in Q4 represents 83% conversion of Adjusted EBITDA. Full-year 2025 FCF totaled $156M .

*Source: Company 8-K *

What Did Management Say?

CEO Adam Anderson highlighted the innovation flywheel and subsea momentum:

"We delivered a strong finish to 2025, with revenues exceeding the high end of our guidance range due to higher-than-expected subsea deliveries, revenue synergies from the DWS and Citadel acquisitions, and new product introductions."

"This is but one example of how our innovation flywheel – powered by deep customer relationships and disciplined execution – enables us to organically expand our footprint with differentiated products that solve meaningful customer challenges."

CFO Kendal Reed emphasized the capital-light model and M&A optionality:

"We converted approximately 83% of our Adjusted EBITDA into Free Cash Flow in Q4 and for the year 2025. We ended the year with approximately $203 million of cash and no bank debt, providing significant financial flexibility as we examine a deep pipeline of inorganic investment opportunities."

Key Strategic Initiatives

Operational Transformation

Innovex made significant progress exiting the legacy Eldridge facility, with full completion expected by the end of Q2 2026 .

CFO Kendal Reed noted: "The expected exit of the Eldridge facility in the second quarter is a foundational element of our plan to improve these margins. We expect a reduced manufacturing footprint, improved on-time delivery, and optimized bidding practices to drive improved subsea margins by year-end 2026."

Subsea Momentum

Innovex reported significant progress in its subsea business :

- XPak Technology: Completed 10th successful installation in Brazil's pre-salt fields; adapted for onshore use in the Permian for a major independent operator

- OneSubsea Alliance: Delivered first subsea wellhead products under the global Innovex-OneSubsea partnership in the Far East

- New Awards: Recently won significant projects in Asia, a smaller award in the Mediterranean, and a landmark subsea wellhead contract in Brazil with an IOC "we have not worked with in over a decade"

- Mexico Completion: Substantially completed deliveries of subsea wellheads and large-diameter tubulars for a major offshore development

CEO Anderson noted: "I'm excited about the trajectory of our subsea business... our subsea strategy is gaining momentum."

Geographic Diversification

Q4 2025 revenue by geography :

International & Offshore accelerated significantly in Q4, with $135M in revenue (+25% QoQ) driven by higher subsea deliveries and product revenues .

Saudi Arabia Expansion: Innovex inaugurated its manufacturing facility in Saudi Arabia during Q4, "further strengthening our commitment to and partnership with the Kingdom" .

M&A Track Record

Innovex has completed multiple acquisitions, most recently Citadel Casing Solutions in May 2025. Recent deals include:

- Nov 2024: Downhole Well Solutions (DWS)

- May 2025: Citadel Casing Solutions

The company maintains a disciplined "small ticket, big impact" approach, with CFO Reed noting they are examining "a deep pipeline of inorganic investment opportunities" while evaluating all investments against the share repurchase authorization .

Balance Sheet & Capital Position

Innovex ended Q4 2025 with a fortress balance sheet :

Management highlighted significant financial flexibility to pursue M&A opportunities aligned with the "small ticket, big impact" strategy, with all investments evaluated against the share repurchase authorization .

Business Model Highlights

Innovex differentiates itself through its capital-light, high-return model:

CEO Anderson describes the approach as an "innovation flywheel – powered by deep customer relationships and disciplined execution" that enables organic expansion with differentiated products .

Product Mix (2025)

Source: Q4 2025 Earnings Materials

Through-Cycle Strategy

Management has consistently highlighted their counter-cyclical playbook:

Up-Cycle:

- Prioritize execution for market share capture

- Expand margins through strategic pricing

- Invest in inventory to support customers

Mid-Cycle:

- Maintain balance sheet strength

- Optimize margins and process improvement

- Continually prune non-core product lines

Down-Cycle:

- Invest while competitors struggle

- Unwind working capital to bolster liquidity

- Evaluate transformative opportunities

"Cycles are a feature, not a bug of the business model. We maintain a fortress balance sheet to allow us to profit from volatility."

Historical ROCE Performance

Source: Company 8-K

The FY 2025 ROCE of 10% reflects higher capital employed (avg. $1.04B) following acquisitions, with income from operations of $133M .

What to Watch Going Forward

- Q1 2026 Results vs. Guidance — Revenue $225-235M and EBITDA $38-42M guided below consensus; watch for execution

- Subsea Margin Improvement — Management expects margins to improve by year-end 2026 as Eldridge exit completes

- Eldridge Facility Exit (Q2 2026) — Full completion of the 80% footprint reduction should drive margin improvement

- International & Offshore Growth — Continued share gains in longer-cycle markets; Saudi Arabia facility now operational

- M&A Pipeline — $203M cash with no bank debt enables opportunistic acquisitions

Related Resources

Last Updated: February 23, 2026 — Includes Q4 2025 8-K press release with Q1 2026 guidance.